The latest headlines are blunt: shipping through the Strait of Hormuz has once again ground to a halt after Washington reportedly moved to physically intercept vessels heading in and out of Iranian ports. At least some ships have already turned around. Maritime analysts now describe the waterway as controlled, unstable, and at rising risk of direct state confrontation. The immediate question is obvious. Is this just another short spike in panic, or the start of something far more serious for oil, shipping, inflation, and everyday life?

First, the Strait Was Never Really Normal

One of the most important points buried beneath the breaking news is that Hormuz has not been functioning normally for quite some time. Several market watchers on Zhihu pointed out that by actual vessel count, daily traffic had already fallen to a tiny fraction of its earlier level. In some periods, transit volume was under 10 percent of the previous norm. By cargo tonnage, the drop looked even worse.

In other words, whether you call it a “complete shutdown” or a “near shutdown” almost misses the point. For energy markets, insurers, refiners and shipping firms, the disruption has already been real for weeks. What changed now is not simply the level of risk, but the number of actors trying to control the chokepoint at the same time.

Why This Matters So Much

The Strait of Hormuz is not just another trade lane. It is one of the world’s key energy arteries. A meaningful share of globally traded crude and liquefied natural gas passes through it. If ships cannot move freely, the shock does not stay in the Gulf. It travels almost immediately into tanker rates, insurance premiums, refinery planning, commodity markets and then consumer prices.

Chinese commentary this week has focused on an uncomfortable reality: even countries that do not directly rely on Gulf oil still feel the price effects. Oil is globally traded. If Asia is suddenly short of supply and willing to pay more, cargoes get rerouted. Traders sell to the highest bidder. That means tightness in one part of the world quickly becomes higher prices in many others, including places that like to think they are insulated.

This is why the current crisis is about more than one waterway or one bilateral standoff. Once enough physical supply is delayed, all benchmarks start speaking the same language: scarcity.

“Hormuz does not need to be 100 percent closed to create a very real global energy shock. It only needs to become dangerous enough that ships, insurers and buyers stop behaving normally.”

Trump’s Logic, and Its Big Problem

One popular line of analysis on Zhihu tried to explain the Trump administration’s thinking in blunt political terms. If Iran keeps using the threat of closing Hormuz as leverage in negotiations, Washington may be trying to neutralize that card by imposing its own external blockade. In simple terms, the message would be: even if Tehran says yes, we can still say no. Even if Tehran says no, we can also decide what happens outside the strait.

It is a classic escalation move. But it also creates a huge contradiction. If the United States wants lower oil prices and less panic, adding a second layer of control may produce the opposite result. Instead of reassuring the market, it can make every shipowner wonder who exactly has authority, who might fire first, and whether a perfectly legal voyage could suddenly become a military incident.

That is why some Chinese observers are skeptical that the blockade can achieve its intended effect quickly enough. A real maritime squeeze on Iran would likely need months to bite. But oil markets, planting seasons, fertilizer demand and domestic political pressure do not wait months politely.

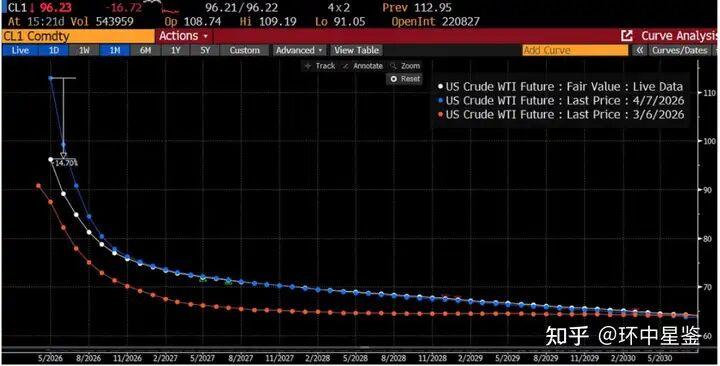

Oil Prices Are Volatile, But the Direction Is Still Up

Another striking pattern in the Zhihu discussion is how often seasoned commodity watchers complained that markets are still underestimating the physical side of this crisis. Prices jump on ceasefire rumors, then fall on diplomatic chatter, then jump again on military headlines. But infrastructure does not recover at tweet speed.

Even if shooting stopped tomorrow, the system would not magically reset. Oil wells shut under emergency conditions can suffer lasting damage. Tanker insurance that surged during wartime does not instantly return to old levels. Congested fleets take time to untangle. Refineries cannot be cold started overnight. And if LNG facilities or port infrastructure have been damaged, repairs can take months or even years.

That is why several Chinese analysts now argue that the market keeps pricing diplomacy by the day while ignoring repair cycles measured in seasons or years. The result is a lot of noise, but an underlying price floor that keeps creeping higher.

Shipping, Fertilizer, Food: The Second Wave of Pain

The first wave of any Hormuz disruption is energy. The second wave is everything energy touches. That means freight, petrochemicals, fertilizers and food. Several of the strongest Chinese responses focused not on Wall Street, but on spring planting and the cost of urea. If diesel and fertilizer stay expensive long enough, the inflation story stops being abstract and becomes agricultural.

This matters especially for import dependent economies with weaker currencies, fragile foreign exchange reserves or heavy external debt. They get hit from several directions at once. Oil becomes pricier. Shipping costs rise. Fertilizer costs rise. Grain imports become more expensive. And governments have less fiscal room to cushion the blow.

In that sense, the real danger is not only a rich world inflation scare. It is the possibility that parts of the developing world face a much harsher combination of energy stress, food stress and political instability.

What About China?

Chinese commenters are split between anxiety and strategic confidence. On the anxious side, higher Asian oil prices are almost taken for granted. On the more confident side, some argue China has more room to adapt than U.S. allies like Japan or South Korea, thanks to strategic reserves, diversified suppliers and a longer term push into green energy.

There is also a very Chinese angle in the discussion: logistics improvisation. Some posts speculate that if maritime disruption drags on long enough, Beijing would accelerate overland energy and trade routes through Pakistan, Afghanistan or Central Asia. Whether those ideas are realistic in the near term is another question. But the discussion itself shows how quickly Chinese public opinion shifts from market reaction to infrastructure thinking.

For expats in China, the immediate takeaway is simpler. Even if China avoids a physical shortage, higher imported energy costs still ripple outward. Transport, aviation, manufacturing inputs, chemicals and food all feel the pressure eventually.

Can the U.S. Actually Enforce This?

Here the skepticism gets sharper. Chinese commentators repeatedly raised three doubts. Can U.S. naval assets operate confidently within range of Iranian missiles? Can Washington really stop ships belonging to major third parties without triggering a bigger diplomatic mess? And can a sustained blockade be managed for months, not just announced for headlines?

These are not small details. If even a handful of ships break through, if escorts appear, or if a U.S. interception ends badly, then the credibility of the blockade comes under instant pressure. One failed demonstration can damage deterrence just as quickly as one successful one can strengthen it.

So while official rhetoric sounds absolute, the actual enforcement picture may be much messier. Markets hate that kind of gray zone. It keeps risk premiums elevated because nobody knows where the real red lines are.

So Where Does Oil Go From Here?

The broad consensus in the Chinese discussion is not that oil goes straight up every day. It is that the baseline has shifted higher and volatility is now part of the story. If tensions cool for 48 hours, crude can drop fast. If a single vessel is intercepted, insurance spikes or a terminal is hit, prices can snap back violently.

More importantly, a lot of analysts no longer believe a ceasefire headline would be enough to send prices back to where they were before the fighting. Too much physical disruption has already occurred. Too much uncertainty remains about repairs, routing, insurance and spare capacity.

Put differently, this is no longer just a headline market. It is a damage market.

Curated and translated from Zhihu, China's largest Q&A platform.

Newsletter

Subscribe to The Expat Edit

Chinese perspectives on global events, wars, and great power competition. Curated from Zhihu.

Free. No spam. View on Substack →