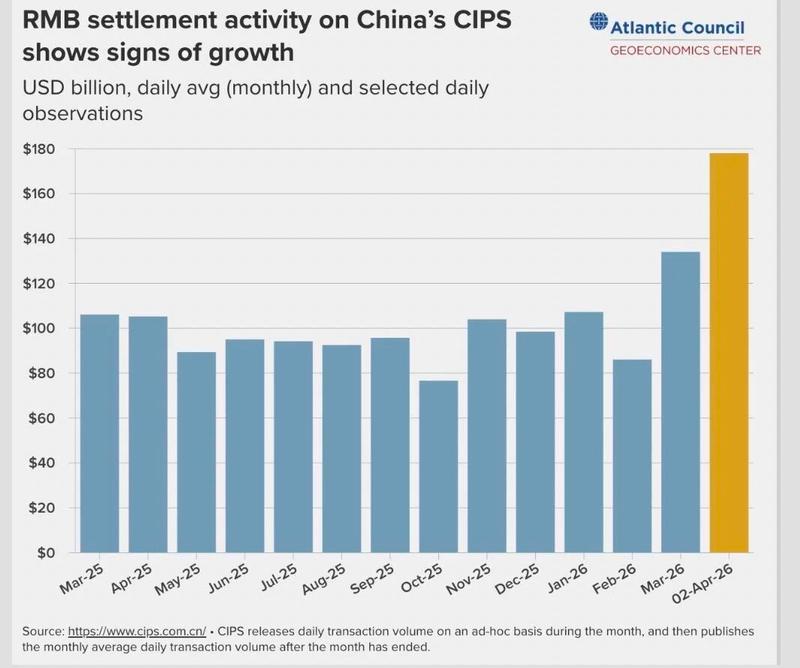

China’s cross-border payment system is suddenly having a very public moment. In March, the RMB Cross-Border Interbank Payment System, better known as CIPS, processed an average of 920.5 billion RMB per day, the highest daily average of the past 12 months. Then on April 2, it jumped again, hitting 1.22 trillion RMB in a single day. The timing is not random. As the US-Israel-Iran conflict rattled global markets, investors started looking for stability somewhere else, and China found itself in an unexpectedly strong position.

What Exactly Happened?

The raw number is what grabbed attention first. One day of CIPS turnover crossing 1.22 trillion RMB is huge by any standard. Official data also showed that March daily average transaction value rose sharply to 920.5 billion RMB, up from 619.7 billion RMB in February. Transaction volume rose too, with March averaging roughly 35,740 transactions per day, compared with about 25,930 in February. By April 2, daily transaction count had climbed to nearly 42,000.

In plain English, more money is moving through China’s own cross-border settlement rails, and it is happening quickly. That does not mean CIPS is replacing SWIFT overnight. It does mean the RMB is becoming more useful in real-world trade and finance at a moment when many countries are actively looking to diversify away from overdependence on one channel, one reserve asset, or one geopolitical bloc.

Why Did the RMB Suddenly Look Attractive?

The bigger story is not just payments. It is what was happening everywhere else. Since late February, after military escalation involving the US, Israel and Iran, markets sold off broadly. Stocks dropped. Gold lost some of its usual shine. Even government bonds in major developed economies took hits as yields rose. When traditional safe havens stop behaving like safe havens, global capital starts scanning the map for alternatives.

China stood out for three reasons. First, Chinese government bond yields were remarkably stable. Second, the RMB strengthened against the US dollar even while several major currencies weakened. Third, China’s policy environment looked more predictable than that of many other large economies. For investors and trade partners alike, predictability matters almost as much as returns when the world feels shaky.

According to reporting cited in Chinese media, some Middle Eastern funds have already flowed into Chinese markets in the short term. That fits a broader pattern. Countries exposed to energy shocks, geopolitical risk, or reserve concentration risk often start rethinking where they hold money, where they borrow, and which currencies they use for settlement.

“This is not just a payments story. It is a confidence story.”

A Stable RMB Helped More Than Headlines Suggest

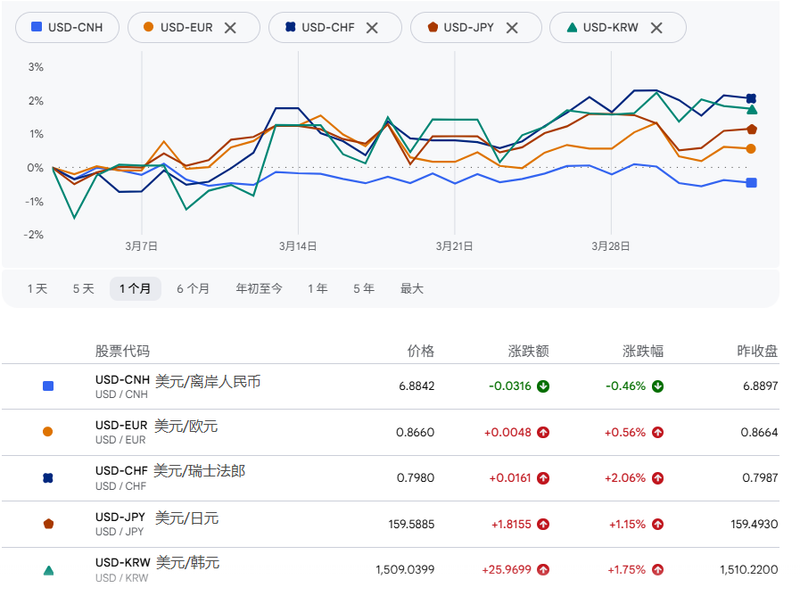

One of the more striking details in the latest coverage is that the RMB was the only major currency to appreciate against the dollar during this recent period, with the onshore rate around 6.8842 per dollar as of April 3. That does not sound dramatic if you are used to stock market fireworks, but in currency markets, that kind of relative stability sends a powerful message.

Compare that with what happened elsewhere. The Japanese yen weakened past 160 against the dollar. The Korean won came under pressure. Even the Swiss franc, usually treated as a classic safe currency, did not shine the way many expected. In that context, the RMB’s resilience looked less like a small technical detail and more like a meaningful signal that Chinese assets were being repriced as a lower-volatility option.

So Is China Becoming a New Safe Haven?

In relative terms, yes, at least for now. Chinese media and several market strategists are increasingly describing China as a new “避风港”, or safe harbor. That claim sounds bold, but the supporting logic is straightforward. China has diversified energy import channels, substantial strategic reserves, a large domestic market, and a policy framework that investors increasingly view as more stable than the alternatives. China also does not currently face the same inflation problem that has complicated monetary policy in much of the developed world.

There is also a structural point worth noting. The RMB’s rise in cross-border use has been built first on trade. That matters. Trade settlement is less glamorous than reserve currency status, but it is usually the more durable foundation. If firms can use RMB to buy oil, machinery, electronics, industrial inputs, or infrastructure services, then the currency becomes more useful even without fully displacing the dollar in global finance.

This is also why it is too simplistic to look at a giant CIPS number and declare the dollar finished. The more realistic interpretation is that global finance is becoming a little more multipolar. The RMB is gaining ground where it makes practical sense, especially in trade-heavy relationships and in regions where countries want more room to maneuver.

What the Viral Takes Get Wrong

Some of the loudest online commentary has taken the 1.22 trillion RMB figure and extrapolated it into sweeping claims about instant RMB dominance. That is not how this works. CIPS is growing fast, but it is still much smaller than the older global plumbing around dollar finance. Also, transaction value does not equal reserve currency supremacy. A payment system can expand rapidly because more trade, financing, and settlements are flowing through it, not because the global order flipped overnight.

At the same time, dismissing the data would also be a mistake. A trillion-RMB day is not noise. It suggests that under stress, a growing number of players are willing to use RMB channels. That is how internationalization tends to happen in real life. Not with one dramatic declaration, but through repeated practical use when conditions make it attractive.

Why Expats in China Should Actually Care

For many foreigners living in China, stories about cross-border settlement systems can sound abstract and very far away from daily life. But the implications are surprisingly tangible. If RMB settlement keeps spreading, it could gradually shape everything from how international businesses invoice clients, to how overseas suppliers trade with Chinese firms, to how global investors think about holding Chinese bonds and Hong Kong RMB products.

It also helps explain a broader shift in tone. A few years ago, conversations around China and money often focused on property stress, capital controls, or slow growth. Now, at least in this particular geopolitical window, the conversation has widened to include China as a source of stability. Whether that perception lasts is another question. But for the moment, the direction of travel is hard to miss.

The real takeaway is not that the RMB has won. It is that the rest of the world is taking it more seriously, especially when volatility makes diversification look smart. CIPS crossing 1.22 trillion RMB in one day is less about one flashy number and more about a larger trend becoming impossible to ignore.

Curated and translated from Zhihu, China's largest Q&A platform. Read the original discussion →

Newsletter

Subscribe to The Expat Edit

Chinese perspectives on global events, wars, and great power competition. Curated from Zhihu.

Free. No spam. View on Substack →